February 27th, 2024

Welcoming 2024 with exciting new features

PropertyMe

Industry News

Vacancy rates decreased sharply in January to 1.1%, rental asking prices continued to rise and February saw a surge in new listing activity.

The residential vacancy rates decreased sharply from 1.3% in December to 1.1% in January, with the total number of vacancies decreasing to 32,108 residential properties.

Decreases in vacancy rates were experienced across all capital cities, with small capital cities, Perth and Adelaide seeing the tightest conditions, with below 1% vacancy rates.

Similarly, CBD areas were affected with Sydney CBD, Melbourne CBD and Brisbane CBD decreases to 4.5%, 3.8% and 2.5% in January.

SQM Research attributes the sharp decrease in vacancies to seasonal trends, driven by increased demand from uni students starting semester one, and graduates entering the workforce.

The vacancy rate has marginally increased by 0.1% when compared to this time last year, highlighting the extended length of Australia’s rental crisis.

Louis Christopher, Managing Director of SQM Research said, “It is a seasonal demand increase we see at the start of each and every year but is most certainly problematic due to the fact the current rental market remains in crisis.

“Going forward, our best-case scenario for renters is that the population growth rate slows considerably this year to an increase of about 360,000 people which would likely mean a stabilisation in rents starting from the June quarter. The worst case is population continues to boom at current rates.”

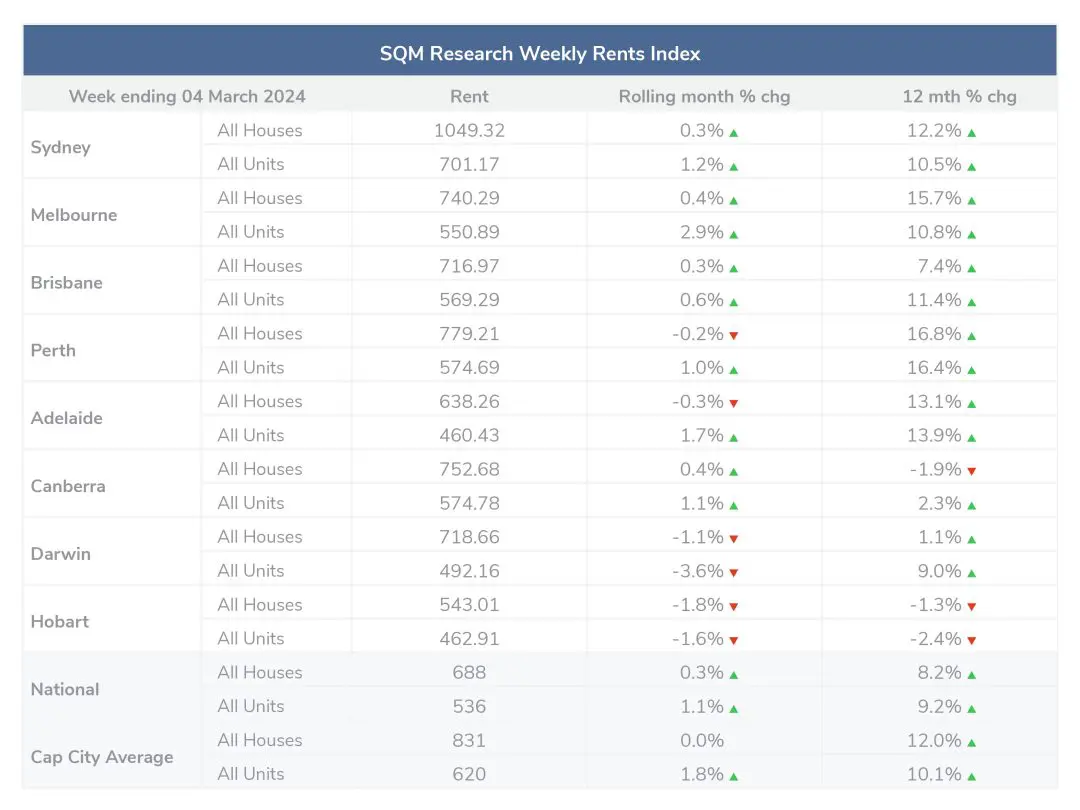

Over the past 30 days to 4 March 2024, national weekly asking prices rose by 0.3% for houses and decreased by 1.1% for units further closing the gap between house and unit pricing. The average national asking price is $688 for houses and $536 for units. Compared to last year, the national asking prices increased by 8.2% for houses and 9.2% for units.

Similarly, across capital cities, the gap between houses and units continues to shorten, across the past 30 days, weekly asking rents for houses have remained steady at an average of $831 per week and units have increased by 2% to $620 per week. Compared to last year weekly asking rents have increased 12% for houses and 10.1% for units.

February has seen significant market activity increases when compared to this time last year and January levels, with an increase in listings across all major cities and an 8.4% increase nationwide from January. New listings increased by 66.4% in February bringing 74,698 new listings to market.

Compared to this time last year, national listings have risen by 3.6%, with Brisbane, Perth and Adelaide bucking the trend with significant decreases of 13.6%, 22.3% and 9.8% respectively.

SQM Research has noted an upward trend in the number of properties sold under distressed conditions, with a 1.1% increase across the past 30 days. An increase in distressed activity was seen in NSW, VIC, NT and TAS.

The national median asking price for houses is $903,485, an increase of 0.3% over the past 30 days, and an 8.8% increase over the past year. The national median asking price for units is $534,714, a 0.8% increase over the past 30 days and a 5.8% increase over the past year.

Median asking prices for capital cities decreased by -0.2% over the past 30 days, however, experienced a 10.4% increase over the past year. Capital city unit prices increased by 0.2% over the past 30 days and 6% for units over the past year.

August saw the RBA hold the cash rate target at 4.35%

The statement by the Reserve Bank board highlighted the following considerations:

While recent data indicate that inflation is easing, it remains high. The Board has indicated that it expects that it will be some time yet before inflation is sustainably in the target range of 2–3 percent in 2025, and to the midpoint in 2026.

Disclaimer: The information enclosed has been sourced from SQM Research and the Reserve Bank of Australia, and is provided for general information only. It should not be taken as constituting professional advice.

PropertyMe is not a financial adviser. You should consider seeking independent legal, financial, taxation, or other advice to check how the information relates to your unique circumstances.

We link to external sites for your convenience. We are selective about which external sites we link to, but we do not endorse external sites. When following links to other websites, we encourage you to examine the copyright, privacy, and disclaimer notices on those websites.